Economy

Related: About this forumMarkets - auto-self-updating embedded graphs: Dow, Oil, Dollar, Pound, Euro. Also: bonds and Listmania

Last edited Fri Apr 11, 2025, 06:31 PM - Edit history (24)

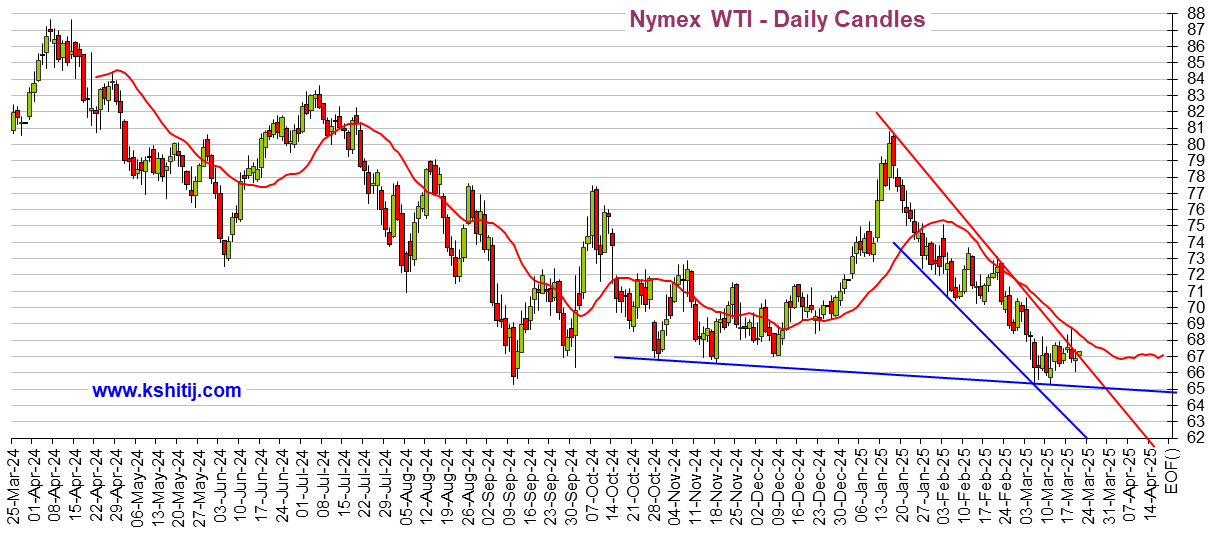

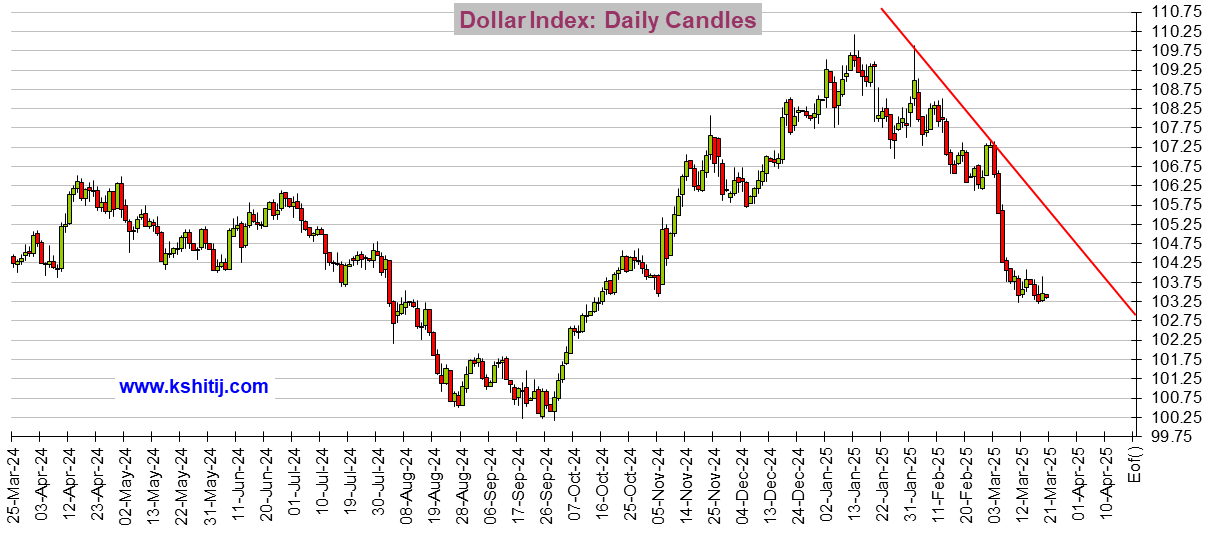

Dow, Oil, and Dollar (last 12 months) - they update a few hours (like about 6 hours) after the close

The graphs above and in the old Stock Market Watch update automatically. So they are up-to-date a few hours after each close.

Click LINKS TO GRAPHS (last Stock Market Watch - but note the graphs update automatically)

Or look above at the top of this OP for the 3 most important graphs:: Dow, Oil, and Dollar (they also update automatically). The other 2 graphs available at the above link are two currencies: the Pound and the Euro

Click bond yields and interest rates (post#4 below)

LISTMANIA

# Better than Biden. Ways EVERYTHING is (NOT) better now, usonian , /111699331

# Notes on the Crises: Currently: Comprehensive coverage of the T&M Treasury Payments Crisis of 2025, usonian, (it's pinned in the Economy Group) /111699437

# NAACP lists companies that dump DEI in its tactical spending guide for Black Americans, BumRushDaShow, /10143397368

# List of DUers on BlueSky, Native, /100220012446

===========================================================================

I always enjoyed scrolling through the graphs to see the trends, THANKS TANSY_GOLD !!!

Fortunately, since they update on their own, we can still see the latest (as of today's close, a few hours after the close) or as of the preceding day's close, even though the SMW is weeks or months old.

Unfortunately the text (e.g. Dow, S&P 500, and Nasdaq) don't update, maybe there's a source for those that can be embedded and updates itself like the graphs, I'm not willing to type these in every day. Maybe weekly at the end of the week. I'll ask General Computer Help for any ideas if somebody doesn't have a solution here.

Myself, I look at the "ribbon of market values" at the top of https://finance.yahoo.com , but I've long been set to the old version of that page, and I'm not sure anyone new to that page see that ribbon of values at the top (or try this, its always had the ribbon : https://finance.yahoo.com/calendar )

S&P 500, Dow 30, Nasdaq, Russell 2000 (small caps), Crude Oil, Gold, Silver, Euro, 10-Year Treasury, Pound, Yen, Bitcoin, XRP (some cryptocurrency thing), FTSE (UK market), Nikkei

Trouble in paradise: Much of the time, after market close, when I click the above finance.yahoo.com or finance.yahoo.com/calendar link, it shows me futures. Sometimes that's what I want. But often I want to see the last closing price. And when the market is open, it shows the current moment's prices. That is usually what I want, but if I'm wanting to see the last closing prices, well, its additional work to get those, one at a time, e.g. click on Dow and then it will put up a page with last closing price and numerous other stats. Repeat above for the S&P 500 ... It's strange that in this day and age everything has to be so damn hard when it could be real easy.

Bonds Here's a mini-page on current yields of Treasuries: 13 week, 5Y, 10Y, and 30Y. https://finance.yahoo.com/bonds/

(The "CBOE Interest Rate 10 Year T No" is just the 10 year treasury yield. Why they couldn't label it "Treasury Yield 10 Years" -- the same as they label the 5 year version "Treasury Yield 5 Years", and the 30 year version "Treasury Yield 30 Years" -- I don't know

For more on bonds, see post#4 .

A few more useful links

GDPNow (estimate of GDP in next quarter) -

Latest Inflation graphs and summary table for all 3 major inflation measures: CPI, PCE, PPI (wholesale prices), both the headline "all items" version and the "core" version. The next update will be when the CPI comes out October 10 (followed by the PPI the next day). If I'm tardy in updating the above link, try my journal, it should be near the top.

FedWatch - CME FedWatch Tool (predicts Feds Fund rates) https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Economic Reports Calendar - https://www.marketwatch.com/economy-politics/calendar MahatmaKaneJeeves thread of this calendar - dunno if the link is permanent, so for now look for it in pinned posts at the top of the Economy Group listings.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

dweller

(26,352 posts)I must have missed an announcement ?

✌🏻

progree

(11,809 posts)The last SMW is the August 30 one that I linked to in the OP.

I did miss that , sorry to see her go .

✌🏻

progree

(11,809 posts)Last edited Sat Mar 15, 2025, 05:54 AM - Edit history (8)

Here's a mini-page on current yields of Treasuries: 13 week, 5Y, 10Y, and 30Y. https://finance.yahoo.com/bonds/(The "CBOE Interest Rate 10 Year T No" is just the 10 year treasury yield).

Yields (3 mo, 6mo, 1Y, 2Y, 5Y, 10Y 30Y, TIPS, Munibonds) Also Fed Funds - this is a more comprehensive listing than the previous, but unlike the previous, it doesn't have links to more info about each. So I list this second https://www.bloomberg.com/markets/rates-bonds/government-bonds/us

Some Treasuries details for those other than 13 week, 5Y, 10Y, and 30Y (listed in the first paragraph above) can be found by formulating the right CNBC URL: for example the 2 Year at https://www.cnbc.com/quotes/US2Y , and the 3 month at https://www.cnbc.com/quotes/US3m etc.

FedWatch - CME FedWatch Tool (predicts Feds Fund rates) https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

===================================================

Bonds don't get much discussion. But financial planners, pundits, etc. are constantly yammering that people should allocate some of their savings to bonds.

Suggested Allocations to Fixed Income and to Equities:

I've seen this one: "Your bonds is your age", i.e. a 60 year old should have 60% in bonds and other fixed income (CD''s, money market, treasury bills, yada), and 40% in equities, but I don't think anyone recommends being that convervative. I think the most common recommendation is, or translates to in effect "your fixed income investments is your age minus ten", i.e. a 60 year old should have 50% in fixed income and 50% in equities.

I'm not that conservative either. Currently I'm targeting "your fixed income investments is your age minus 30", so a 60 year old would be 30% in fixed income and 70% in equities. (I'm more like 70 years old, so 40% in fixed income and 60% in equities).

Schwab has a confusing suggested allocation: For age early 60's: 60% stocks, 40% Fixed Income (FixedIncome=age-20);; Early 70's 40% stocks, 60% Fixed Income (FixedIncome= age-10 ). 80+: 20% in stocks, 80% in Fixed Income . https://www.schwab.com/retirement-portfolio

And then there is the record of bonds in the last 5 years:

I sometimes use VCOBX, Vanguard Core Bond Fund, as an indicator ( https://www.morningstar.com/funds/xnas/vcobx ).

. Click on Interactive Chart (or go to https://www.morningstar.com/funds/xnas/vcobx/chart ). I selected 5 years to get back before the pandemic (one can also adjust the start dates and end dates. The default FREQUENCY is Monthly, I changed it to Daily. From 9/11/2019 to 9/12/2024, a $10,000 bond investment grew to $10,595, a 5.95% increase over 5 years (which works out to an annualized average of 1.16%/year). This is total return including reinvested dividends.

At least it's positive, albeit microscopic. Unfortunately, after inflation which was 22.7% during that period [1], it would be a 13.7% drop. Meaning one's $10,000 VCOBX nest egg 5 years ago would have about $8,630 in purchasing power today.

If one were unfortunate enough to have bought this bond fund in early January 2021, for example, it would have been a negative 4.1% return over the nearly 4 years in nominal dollars, and a 22% drop in purchasing power after adjusting for inflation.

This is an intermediate bond fund. It would have been worse for a longer-term bond fund (and not as bad for a shorter term bond fund)

That said, the situation will improve when interest rates drop. For example from 10/20/23 to 9/12/24, VCOBX gained 14.6% in these 11 months before adjusting for inflation (which was only 2.2% cumulative over 11 months). During that period, the 10 Year Treasury yield, for example, dropped from 4.92% to 3.68%. The 5 Year Treasury yield dropped from 4.62% to 3.47%. The 2 Year Treasury Yield ( https://www.cnbc.com/quotes/US2Y ), seen as sensitive to monetary policy, went from 5.00% to 3.57% during that period.

(The Federal Reserve's Fed Funds rate stayed essentially the same during that period -- targeted at a 5.25 to 5.50% range and effectively 5.33%).

By way of comparison to U.S. equities, $10,000 in VFIAX, the S&P 500 index fund, increased 102% over the 5 year period 9/11/2019 to 9/12/2024 (that's a 2.02 fold increase), and about 65% after inflation, to $16,500 in purchasing power, nearly double (1.91 X) the VCOBX investment purchasing power.

30 Year Record:

In the longer term, like 30 years from the end of 1989 to the end of 2019, a $10,000 investment in 10 Year Treasuries would have grown to $56,035, while the same $10,000 invested in the S&P 500 would have grown to $168,536. Based on data at https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

In the 30 year example, I deliberately chose a period that was pre-pandemic. For the most recent 30 year period covered in the table, from the end of 1993 to the end of 2023, $10,000 in 10 Year Treasuries would have grown to $33,359, while the same $10,000 invested in the S&P 500 would have grown to $176,926.

The stern.nyu.edu page above also has investments in 3 month T bills and Baa corporate bonds. Maybe when I'm in the mood, I will do the 30 year calculations for these. It also has investments in real estate and gold.

That said, the vast consensus is that stocks in aggregate are overpriced, often citing the very high Case Shiller CAPE ratio. As a consequence, the Vanguard Capital Markets Model, 8/29/24, forecasts equities to average an annualized: 4.2% +/- 1.0% over the next 10 years, and for bonds about 5%. https://corporate.vanguard.com/content/corporatesite/us/en/corp/vemo/vemo-return-forecasts.html

Fidelity or Schwab recently published a similar forecast, its on my to-do list to hunt for that link

-----------------------------------------------

[1] Inflation CPI: https://data.bls.gov/timeseries/CUSR0000SA0 . The latest is August 2024, so I used August 2024 over August 2019 in this calculation (the main thing is the period length be 5 years). For the January 2021 hypothetical bond purchase, I used August 2021 over December 2020.

progree

(11,809 posts)Last edited Sat Apr 12, 2025, 05:46 PM - Edit history (2)

and volatile. A good graph of that volatility, e.g. Vanguard IntermediateTerm Treasury Admiral VFIUX

https://www.morningstar.com/funds/xnas/vfiux/performance

(Updated below for 4/11/25 ending value. Later: updated the time frame to a more accurate 10.2738 years)

plus a table of total annual returns by year. Negative numbers are in parenthesis ( )

2015 1.61%

2016 1.29%

2017 1.67%

2018 1.10%

2019 6.39%

2020 8.31%

2021 (2.19%)

2022 (10.34%)

2023 4.18%

2024 1.48%

YTD 2.10%

which shows some of the volatility and the piss-poor returns.

Since the beginning of 2015, its total return is cumulatively only 15.39%

(A $10,000 investment grew only to $11,539 in those 10.2738 years)

which comes to an average annualized total return of only (1.1539^(1/10.2738) -1)*100% = 1.403%/yr

And as far as purchasing power, it is way underwater:

CPI: https://data.bls.gov/timeseries/CUSR0000SA0

1/2015: 234.747

3/2025: 319.615

So, consumer costs rose 36.15% during that period.

The purchasing power of the $10,000 bond portfolio is now only $8,475 (=234.747/319.615 * $11,539), a 15.2% decrease.